The Lesson No School Teaches, But Every Parent Can

Every Indian parent invests deeply in their child’s education: tuition, coaching classes, extracurriculars, and college preparation. Yet there is one subject almost no school teaches and no syllabus addresses: how to manage money.

Children in India grow up watching their parents earn, spend, and occasionally stress about money, but rarely with any structured conversation about what money is, how it works, and how their choices with it will shape their adult lives.

The result is predictable. Young adults enter their first jobs with excellent academic qualifications and very little financial literacy. They earn well, spend impulsively, save irregularly, and build wealth slowly, because nobody taught them the fundamentals when it mattered most.

Financial education for children does not require a finance degree, a large corpus, or a formal classroom. It requires consistent, age-appropriate conversations and activities, starting as early as age 3 and building layer by layer through adolescence. The habits formed in childhood become the financial instincts of adulthood.

Here are 9 practical strategies for teaching children about money in India, with age guidance, real examples, and steps you can start this week.

Why Financial Education for Kids Matters More Than Most Parents Realise

Financial habits and attitudes formed in adulthood are largely rooted in childhood. Research by behavioural economists shows that children’s financial behaviours: their saving instincts, their attitude to delayed gratification, their sense of value, all of these are shaped between ages 7 and 14 and persist through adult life.

A child who learns to save toward a goal at age 8 grows into an adult who saves toward retirement at 28. A child who understands that debt has a cost at age 12 grows into an adult who reads credit card terms carefully at 24.

| The Cost of Starting Late: An Illustration. Two cousins, same family, same income. Aryan (financially educated from childhood) starts a Rs. 5,000 per month SIP at age 22. Rajiv (no financial education) starts the same SIP at age 32. Aryan at age 60 (38-year SIP at 12%): approximately Rs. 3.2 crore.Rajiv at age 60 (28-year SIP at 12%): approximately Rs. 1.4 crore. The 10-year head start is worth Rs. 1.8 crore. That difference is the cost of financial illiteracy, paid not in rupees, but in time. |

Age-by-Age Financial Education Roadmap

Financial education works best when it is age-appropriate and progressive. Each concept builds on the last.

| Age | Stage | Key Concepts | Practical Activities |

| 3 to 5 | Toddler | Needs vs. Wants. Coins have value. Waiting is okay. | Play shop at home. Count coins. Use a clear piggy bank. |

| 6 to 8 | Early Primary | Earning via small tasks. Saving toward a goal. Spending decisions. | 3-jar system (Spend/Save/Give). Weekly pocket money. First savings goal. |

| 9 to 12 | Upper Primary | Budgeting basics. Comparing prices. Income and expense. | Monthly pocket money with expense tracking. First bank account. Visit the bank together. |

| 13 to 15 | Early Teen | Interest and compounding. Loans and debt. How banks work. | Open a savings account jointly. Explain the FD interest. Show compound interest visually. |

| 16 to 18 | Late Teen | Mutual funds. Tax concept. Career-income link. | Show your portfolio. Open a minor investment folio. Discuss SIP compounding. |

| 18+ | Young Adult | First job finances. Credit score. EPF. Insurance. First investment. | First SIP in their own name. Term insurance discussion. Joint goal planning. |

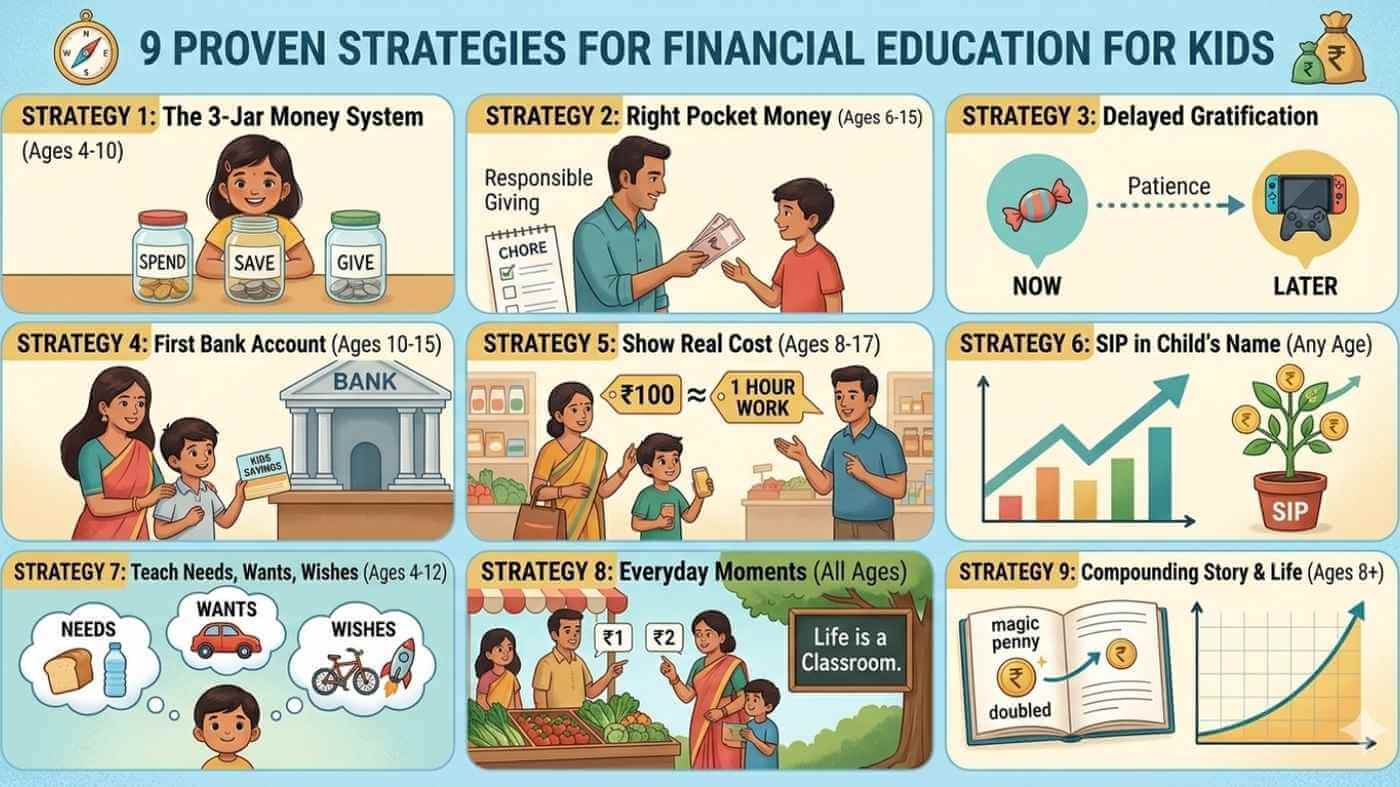

The 9 Strategies for Financial Education for Kids

Strategy 01: The 3-Jar Money System (Ages 4 to 10)

Give your child three transparent jars, labelled Spend, Save, and Give. Whenever they receive pocket money or birthday money, they divide it: 60% Spend (small daily wants), 30% Save (a specific goal), 10% Give (chosen by the child). When the Save jar reaches the goal, celebrate visibly and start a new one immediately.

The 3-jar system makes abstract financial concepts physical and visible. Children learn that money has purpose and that every rupee should be assigned a role. The Give jar introduces generosity and value beyond consumption, shaping financial character for life.

Parent Tip: Do not rescue the Spend jar. If your child runs out before the week ends, that experience is far more valuable than any lecture about budgeting. Resist the temptation to top it up.

Strategy 02: Give Pocket Money the Right Way (Ages 6 to 15)

Regular, predictable pocket money is the foundation of childhood financial learning. It creates conditions for real financial decisions without the stakes of adult life. Set a weekly or monthly amount appropriate to age: Rs. 30 to 50 per week for ages 6 to 8, Rs. 100 to 200 per week for ages 9 to 12, Rs. 300 to 500 per month for ages 13 to 15.

Give the child genuine autonomy over their spending portion. No questioning their choices. Tie a small portion to age-appropriate household contributions. Not payment for every task, but a recognition that contribution and income are connected.

Parent Tip: The most important rule: never advance pocket money or bail out a child who overspends. The discomfort of running out is the most powerful financial lesson in the childhood curriculum.

Strategy 03: The Delayed Gratification Exercise (Ages 5 to 14)

When your child wants something they cannot immediately afford, resist buying it. Help them calculate how many weeks of saving it will take. Write the goal on a chart with a visual tracker: colour a box for every week of savings. When they reach the goal and buy the item themselves, the satisfaction is entirely different from a parental purchase.

Decades of research, including the Stanford marshmallow experiments, have shown that the ability to delay gratification in childhood is one of the strongest predictors of adult financial success. For older children, introduce the 30-day rule: if they still want something after 30 days, it is a real desire, not an impulse.

Parent Tip: Your biggest challenge is enduring the child’s impatience without caving. Stay firm, stay warm, and stay enthusiastic about the goal. Your emotional engagement matters as much as the lesson.

Strategy 04: Open Their First Bank Account Together (Ages 10 to 15)

Most banks in India allow minor accounts from the age of 10. Take your child to the branch, let them fill out the form with your guidance, and make the first deposit themselves. Show them how to use internet banking or a passbook. Let them track the balance monthly.

A bank account transforms money from coins and notes into a system. It introduces balance, interest, deposits, and withdrawals in a completely practical, hands-on way. Even a small interest credit of Rs. 3 or Rs. 4 is exciting when a child sees their money make more money while sitting still.

Parent Tip: Avoid over-managing the account. Let them experience the growth and the occasional temptation to withdraw. The decisions they make with their own account are vastly more educational than watching you manage yours.

Strategy 05: Show the Real Cost of Things (Ages 8 to 17)

For younger children, show them that a Rs. 500 toy costs Mama or Papa a certain number of working hours. For older children, share the actual household budget in round numbers: rent, groceries, EMIs, and school fees. Let them calculate what percentage of their monthly income each expense represents.

Children who understand the connection between work, time, and money develop a fundamentally different relationship with spending. The concept of ‘this costs how many hours of work’ makes price tags meaningful in a way that abstract rupee values do not.

Parent Tip: Share enough to make money real and meaningful, but do not create financial anxiety. Frame it positively: this is how our family uses money wisely.

Strategy 06: Start a SIP in Your Child’s Name (Any Age)

Open a minor mutual fund folio in your child’s name with you as guardian. Start a small SIP. Even Rs. 500 to Rs. 1,000 per month is enough for educational purposes. Choose a NIFTY 50 index fund or a balanced fund for simplicity and stability. Show your child their portfolio on every anniversary. Explain what happened during any significant market movement.

When a child sees their investment portfolio grow over the years, experiences a correction and a recovery, and watches compounding work in real rupees, the abstract concepts of investing become deeply personal. No classroom can replicate this learning. When your child turns 18, the folio converts to their name, a meaningful wealth gift, and the beginning of their adult investment journey.

A good place to start is a conversation with VSJ FinMart. We help parents open minor investment folios, choose a suitable fund for the child’s education horizon, and explain compounding in a way that makes sense to both parent and child.

Parent Tip: Make the SIP a shared experience, not a parental secret. Show your child the account periodically. Let them ask questions about why the value went up or down. These conversations are more valuable than the corpus itself.

Strategy 07: Teach Needs, Wants, and Wishes (Ages 4 to 12)

Play the sorting game. Give children a list of items or cut out pictures from catalogues. Ask them to sort each into three piles: Need (must have to survive or function), Want (would like but can live without), Wish (wonderful but not planned for yet). Discuss the borderline cases together: is a new cricket bat a need or a want?

Children who cannot distinguish between these categories grow into adults who overspend on wants while under-investing in needs. The distinction sounds obvious to adults but is genuinely non-obvious to children, who experience desire and necessity with similar emotional intensity.

Parent Tip: Do not judge your child’s categorisation. The goal is for them to develop their own evaluative framework, not to adopt yours. Ask open questions: why did you put that in Wants?

Strategy 08: Use Everyday Moments as Financial Classrooms (All Ages)

At the grocery store, let children compare prices and choose the better value. At Diwali, include them in the gift budget conversation. When paying bills, briefly explain what each bill is for. When making a big purchase, narrate your decision-making process out loud.

The most powerful financial education happens in ordinary situations, not scheduled lessons. Parents who narrate their financial decisions in child-appropriate language create continuous, contextual learning that no formal curriculum can replicate. Children learn by watching, listening, and eventually participating.

Parent Tip: Financial narration is a habit, not an event. Start with one or two everyday moments this week. Over months, it becomes natural, and your child absorbs financial thinking as a normal part of daily life.

Strategy 09: Teach Compounding with a Story, Then Show It in Real Life (Ages 8+)

Tell the rice-and-chessboard story: a king promised a sage any reward. The sage asked for one grain of rice on the first square of a chessboard, two on the second, four on the third, doubling each time. The king laughed, then discovered the total exceeded all the rice in the world. That is what your investment does.

Then show it happening. Open your child’s SIP statement and show them what Rs. 500 per month has grown to so far, and what it will grow to in 10, 20, and 30 years using an online SIP calculator. Children intuitively understand the magic when they type in the numbers and see the result themselves.

Parent Tip: The story matters. The visual calculator matters even more. Use the SIP calculators on the AMC websites together. Let them play with different starting ages and amounts. The lesson is most powerful when they discover it themselves.

The Power of Starting Early: A Compounding Gift for Your Child

Here is what a modest annual investment of Rs. 5,000 (birthday money, Diwali money, or a small annual gift can grow to at 12% per annum in an equity mutual fund SIP. Same amount invested, same rate. Only the starting age changes.

| Start Age | Annual Gift | Horizon | Total Invested | Approx. Corpus at 60 |

| Age 5 | Rs. 5,000/year in equity MF SIP | 55 years | Rs. 2.75 lakh | Rs. 1.4 crore |

| Age 10 | Rs. 5,000/year in equity MF SIP | 50 years | Rs. 2.50 lakh | Rs. 84 lakh |

| Age 18 | Rs. 5,000/year from 18th birthday | 42 years | Rs. 2.10 lakh | Rs. 48 lakh |

| Age 25 | Rs. 5,000/year from first job | 35 years | Rs. 1.75 lakh | Rs. 26 lakh |

| The Most Powerful Number in This Table: Starting at age 5 vs. age 25: same Rs. 5,000 invested annually. Corpus difference: Rs. 1.4 crore vs. Rs. 26 lakh. More than Rs. 1.1 crore created purely by 20 extra years of compounding. No additional money. No smarter investment. Just time. This is the gift that financial education gives your child: the understanding to use time before it runs out. |

India-Specific Financial Products for Children

These are the key products available in India designed for or well-suited to children’s financial education and wealth building.

| Product | Eligible Age | Why It Teaches | Where to Open |

| Post Office Savings Account | Ages 10+ | Banking basics in a safe, government-backed environment. Passbook makes balance visible. | Any Post Office |

| Minor Savings Bank Account | Ages 10+ | A child can operate independently after the age of 10 in most banks. Teaches deposits, withdrawals, and interest. | Home branch of your bank |

| Sukanya Samriddhi Yojana | Girl child up to age 10 | Government scheme for girls. 8.2% p.a. (current rate). Section 80C benefit. Teaches long-term goal saving. | Post Office or authorised banks |

| Minor Mutual Fund Folio | Any age (parent as guardian) | Units held in the child’s name. Converts to regular folio at 18. Teaches long-term investing from childhood. | Any AMC or AMFI-registered distributor |

| PPF Account (Minor) | Any age (parent operates) | Currently 7.1% p.a., fully tax-free. Long lock-in teaches patience and consistency. | Post Office or SBI |

| Recurring Deposit (RD) | Ages 8+ | Fixed monthly contribution, guaranteed returns. Good first savings product for building the habit. | Any bank or Post Office |

5 Common Mistakes Parents Make in Children’s Financial Education

Mistake 1: Shielding Children from Money Reality

Many Indian parents avoid money conversations with children to protect them from worry. However, children who are never exposed to financial concepts develop anxiety and confusion about money in adulthood, precisely because it remains mysterious and unexamined. Age-appropriate transparency is far healthier than protective silence.

Mistake 2: Using Money as Reward or Punishment

Paying children for every small task, or withholding pocket money as punishment for behaviour, trains them to see money as a behavioural carrot-and-stick rather than a tool for life management. Good behaviour should be rewarded with praise, not rupees. Pocket money should be predictable and mostly unconditional.

Mistake 3: Rescuing Children When They Run Out of Money

Every time a parent advances pocket money or silently covers a child’s shortfall, they remove the most powerful financial lesson available: the natural consequence of overspending. Let the jar run empty. Let them wait until pocket money day. The discomfort is the curriculum.

Mistake 4: Investing for Children Without Telling Them

Many parents open Sukanya accounts, PPFs, or child education SIPs with good intentions, and never tell the child. These investments become surprise adult discoveries rather than childhood education tools. Tell your child about every investment made in their name. Show them the statements. Make them stakeholders in their own financial future.

Mistake 5: Waiting Until They Are Old Enough

There is no age at which financial education is too early. A 3-year-old can learn that coins are traded for things. A 5-year-old can understand that money can run out and that waiting is rewarding. The earlier you begin, the more deeply the lessons embed. There is no perfect starting age. There is only sooner and later.

The Richest Legacy You Can Leave Is a Financial Mind

The investments you make in your child’s name will be meaningful. The investment you make in your child’s financial understanding will last a lifetime, long after any SIP corpus has been spent and any inherited wealth has been redistributed.

Children who grow up understanding money (who have held it, counted it, spent it badly, saved it patiently, and watched it grow) become adults who manage wealth thoughtfully and make decisions from confidence rather than anxiety.

Start with one jar. Start with one conversation. Start this week. The compounding of financial wisdom, like the compounding of money, begins with the first rupee.

If you want to open a mutual fund folio in your child’s name and build a goal-based investment plan around it, VSJ FinMart can help you set it up from scratch, choose the right fund for your child’s timeline, and review it together every year.

Frequently Asked Questions

At what age should I start teaching my child about money in India?

Financial education can begin as early as age 3 to 4 with very simple concepts: coins have value, things cost money, and you can save up for something you want. The 3-jar system works well from age 4 to 5. Regular pocket money and savings goals are effective from age 6 onwards. Banking concepts suit ages 10 to 12. Investment concepts such as mutual funds and compounding can begin at age 12 to 14 with parental guidance. There is no age too early: every concept simply needs to be adapted to the child’s developmental stage.

How much pocket money should I give my child in India?

A general guide: Rs. 30 to 50 per week for ages 6 to 8; Rs. 100 to 200 per week for ages 9 to 12; Rs. 300 to 500 per month for ages 13 to 15. The amount matters less than the predictability, autonomy, and consequences that come with it. Never advance pocket money or bail out a child who overspends: the experience of running out is the most valuable financial lesson at this stage.

What is the best investment product for a child in India?

The right product depends on the goal. For long-term wealth creation over 15 to 20 years, a minor mutual fund SIP in an equity index fund offers strong growth potential, with the added benefit of teaching compounding and market behaviour. For a girl child specifically, the Sukanya Samriddhi Yojana provides government-backed returns at 8.2% per annum with Section 80C benefits. For capital safety with steady growth, PPF in the child’s name offers 7.1% per annum tax-free. For teaching banking basics, a minor savings account is the right starting product. Speak with a registered AMFI distributor to match the right product to your child’s goal and your family’s circumstances.

How do I explain compounding to a child?

Start with the rice-and-chessboard story: a king promises a sage rice that doubles on each square of a chessboard. By the 64th square, more rice than exists in the world. Then use an online SIP calculator together and let your child type in Rs. 1,000 per month starting at age 10, and see the projected corpus at age 60. The calculator does the explaining. Follow up by showing them their own investment account and explaining how the money grew without them doing anything except leaving it invested.

What are the most common mistakes parents make in children’s financial education?

The five most common mistakes are: shielding children entirely from money realities, which creates adult financial anxiety rather than preventing it; using money as reward or punishment for behaviour; rescuing children when they run out of pocket money, removing the most valuable natural consequence; investing for children without involving them, missing the entire educational opportunity; and waiting until the child is old enough, when earlier is always better. The ideal approach involves age-appropriate transparency, consistent systems, natural consequences, and children as active participants in their own financial education.

Disclaimer

The information provided in this blog is for educational and informational purposes only and should not be construed as investment advice. Please consult a qualified financial advisor before making any investment decisions. Shashikant Chanderkumar Mudaliar (ARN: 319377), operating under the brand name VSJ FinMart, is an AMFI-registered Mutual Fund Distributor (MFD) and does not provide investment advisory services. Mutual fund investments are subject to market risks. Past performance is not indicative of future results. All return figures mentioned are illustrative estimates based on historical data and are not guaranteed. Interest rates and product terms for government schemes (Sukanya Samriddhi Yojana, PPF) are subject to revision. Please verify current terms before investing. Please read all scheme-related documents carefully before investing. Registration details can be verified at www.amfiindia.com/locate-distributor.